Key takeaways

- The 4% rule is a useful starting point, but not a guarantee, which is why you should always review your plan regularly.

- Inflation, market sequence, and taxation have a greater impact on portfolio longevity than average returns alone.

- Flexibility, behavioral steadiness, and coordinated tax planning can extend portfolio life well beyond expectations.

Retirement today lasts longer than ever. For many Americans, it spans thirty years or more, stretching across multiple market cycles, tax regimes, and phases of life. What once felt like a simple question — “How much can I withdraw each year?” — now invites a complex answer.

Here’s a stat from Fidelity that’s worrisome: Nearly one in five retirees spends faster than planned during their first five years of retirement.

It isn’t usually investment performance that determines success or failure. It is withdrawal behavior — how much, when, and from where those funds are drawn.

The classic “4% rule” provided a helpful framework in the 1990s, but its assumptions no longer fully reflect today’s environment. With lower bond yields, longer lifespans, and higher healthcare costs, retirees now require a more flexible and personalized approach. The goal is not a fixed number, but an adaptable system that keeps your portfolio — and your lifestyle — sustainable through time.

Revisiting the 4% Rule in a Modern Context

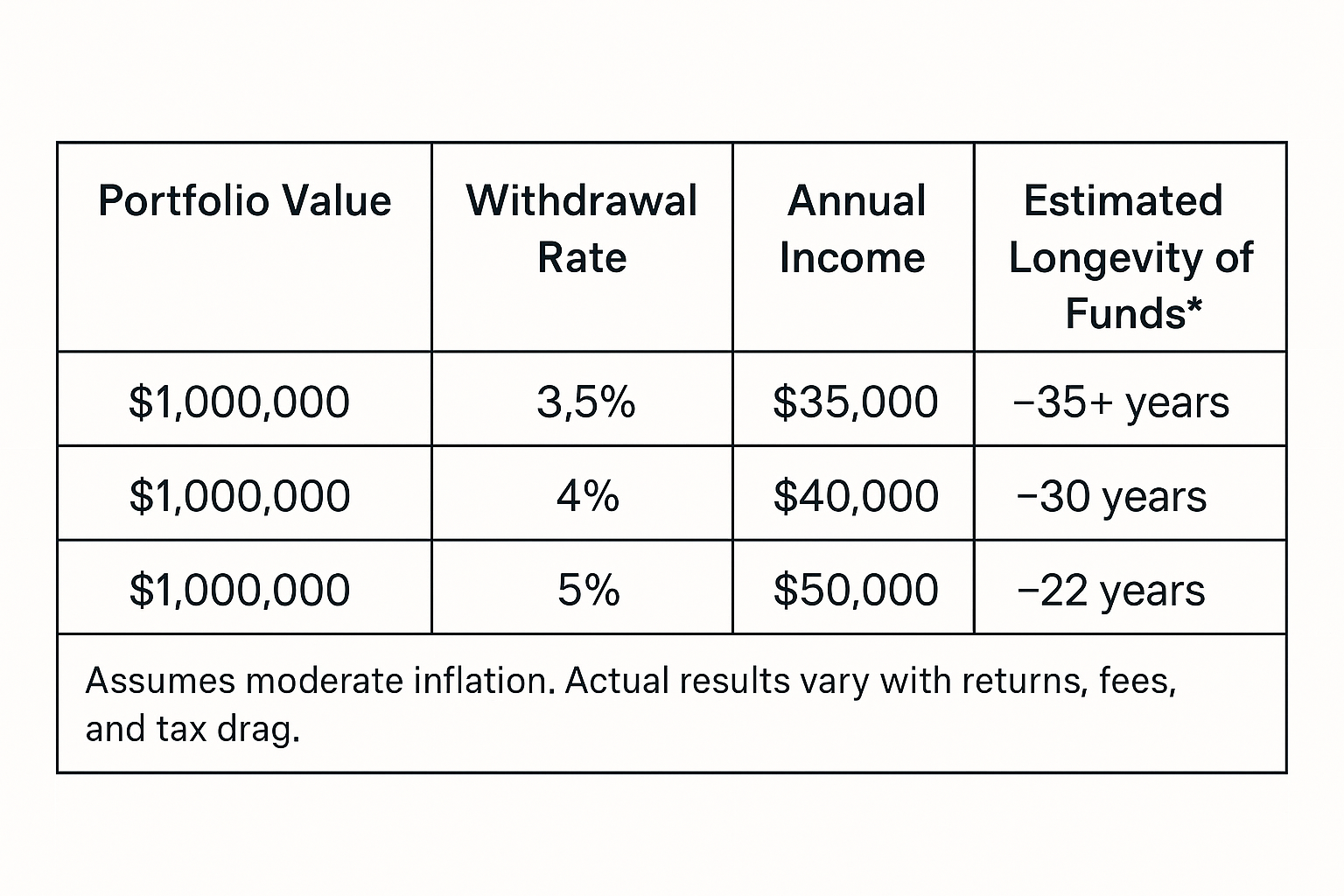

A withdrawal rate is simply the portion of your investment portfolio you draw each year for income. In 1994, financial planner William Bengen analyzed historical returns and concluded that withdrawing 4% in the first year of retirement — increasing that amount annually for inflation — had a high likelihood of lasting thirty years.

That finding became known as the “4% rule.” It was built on several assumptions: a 60/40 stock-bond portfolio, moderate inflation, and an investment horizon of about three decades.

Today, those foundations have shifted. Bond yields remain subdued, inflation has been more variable, and retirees often live longer than the thirty-year model assumed. Many current analyses suggest a starting range closer to 3–3.5% may better reflect today’s conditions for conservative investors, while more flexible or equity-heavy portfolios may support up to 4.5–5%, provided withdrawals adjust to market performance.

The table illustrates the essential trade-off: higher withdrawals provide more income now but reduce long-term durability. The “right” rate is therefore not fixed but tailored — reflecting health, tax situation, and willingness to adjust spending when conditions change.

The Real Forces That Determine Portfolio Longevity

- The Sequence of Returns

The order in which gains and losses occur matters more than the average return itself. A retiree facing a 20% market decline early in retirement will deplete assets faster than one encountering the same decline later. Managing this risk requires keeping adequate reserves and resisting emotional selling. - Inflation and Rising Costs

Even moderate inflation quietly erodes purchasing power. At 3% inflation, $100,000 in expenses today would require $134,000 a decade from now. Healthcare costs often outpace this rate, making real-world spending more demanding than projections suggest. - Longevity and Health

A 65-year-old couple has about a one-in-four chance that one partner lives past 95. That reality pushes many planners to test portfolios for 35–40 years rather than 30. Long-term care, now averaging over $100,000 annually, remains the largest unplanned expense for many retirees. - Behavior and Discipline

Investment success depends not only on markets but on temperament. Panic selling, overspending early in retirement, or holding unrealistic return expectations all shorten portfolio life. Behavioral steadiness, particularly during volatility, is a defining advantage. - Taxes, Fees, and Policy Shifts

Returns are measured in after-tax, after-fee terms. The scheduled 2026 sunset of several provisions from the Tax Cuts and Jobs Act, along with SECURE 2.0 changes to RMDs and estate exemptions, will alter how income and inheritance are taxed. Withdrawal planning that integrates these factors can significantly extend portfolio endurance.

Constructing a Withdrawal Strategy That Adapts

Dynamic Withdrawal Models

Rather than fix withdrawals to an inflation-adjusted percentage, dynamic models respond to portfolio performance. Spending may decrease modestly after poor market years and rise after strong ones. This approach increases the likelihood of long-term success without requiring constant austerity.

Layered “Bucket” Approaches

Segmenting assets by time horizon helps balance stability and growth. One structure may hold two years of living expenses in cash equivalents, five years in conservative bonds, and the remainder in equities for long-term appreciation. A retiree with $1.2 million in 2025 could use this structure to fund short-term needs while allowing the growth bucket to recover after downturns.

Tax-Efficient Sequencing

Drawing income in the right order often matters more than the amount. Taxable accounts typically come first, followed by pre-tax retirement accounts, and finally Roth assets. This helps control annual tax brackets, manage Medicare premiums, and reduce required minimum distributions later.

Creating a Reliable Income Floor

Partial annuitization or guaranteed pension income can secure essentials such as housing and insurance, allowing investment accounts to serve discretionary goals. For many retirees, psychological comfort improves dramatically once the basics are covered by predictable income.

Establishing Guardrails

Guardrail strategies set upper and lower limits for withdrawals. When portfolio values rise, withdrawals increase within limits; when they fall, distributions are trimmed proportionally. This keeps spending aligned with market conditions without forcing constant recalculation.

Testing and Recalibrating Over Time

No plan survives unchanged. Each year brings new data, new prices, and new legislation. Running updated projections through Monte Carlo simulations or similar stress tests helps reveal how a plan holds up across hundreds of possible market paths.

Two retirees with identical savings might require entirely different withdrawal strategies depending on tax structure, investment fees, healthcare assumptions, or legacy goals. Annual review ensures these variables remain in harmony. A fiduciary advisor’s responsibility is to measure — not guess — the tolerance your plan has for change.

Course Corrections During Retirement

Even well-built plans need adjustment. If withdrawals prove too aggressive in early years, retirees can restore balance by delaying Social Security, trimming non-essential spending, or purchasing a partial income annuity. Conversely, if conservative withdrawals leave excess funds unspent, those assets can support philanthropy, family assistance, or travel later in life.

Flexibility is not a sign of uncertainty; it is a safeguard. Portfolios that adjust intentionally to life’s changes often outlast those that remain rigid.

The Psychology of Spending After a Lifetime of Saving

Retirement is not merely a financial transition — it is a behavioral one. After decades of accumulation, many retirees struggle to shift toward mindful spending. The instinct to preserve capital, even when it’s no longer necessary, can limit enjoyment and create unwarranted anxiety.

Once a withdrawal strategy has been validated and stress-tested, purposeful spending becomes an act of confidence, not indulgence. The purpose of financial security is to live freely within reason, not to postpone fulfillment indefinitely.

A Life Designed to Endure — and Be Lived

There is no single percentage that guarantees financial safety for the next thirty years. The 4% rule remains a useful benchmark, but every retirement plan must evolve with its owner’s life, health, and priorities.

Running out of money is a genuine risk. So is reaching the end of life with unused wealth and unlived experiences. The art of planning lies in balancing both.